- Features

- Money Management

- Financial GoalsSet a goal to make sure it is achievable and fits your budget using SMART

- PaceMonitor your money flow speed in real time to stay ahead of overspending

- Monthly Expense TrackerAccess a month-end snapshot of your Plan to understand financial habits clearly

- Leftover MoneyAlways know how much spending money you have after budgeting for necessities

- Net Worth TrackerUse several data connectors to track your net worth

- Expense Tracking

- TransactionsSee all transactions from all of your financial institutions in one list

- Spending InsightsAnalyze your tracked spending data to better adjust your budget

- Cash Flow TrackerTrack your profit or deficit by analyzing your recurring and variable expenses

- Transaction RulesAuto-organize and customize your finances in seconds to reclaim your time

- Debt & Bills

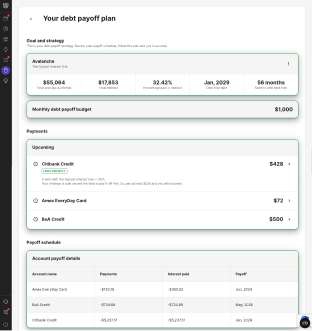

- Debt Payoff PlannerYour personal payoff schedule based on the strategy and budget

- RecurringManage all your bills and subscriptions in one place

- Cancel SubscriptionsFind unwanted subscriptions you would like to cancel and save your money

- Lower Your BillsNegotiate better rates for your cell phone or cable bills with Billshark

- Money Management

- Calculators

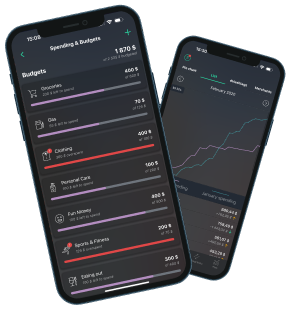

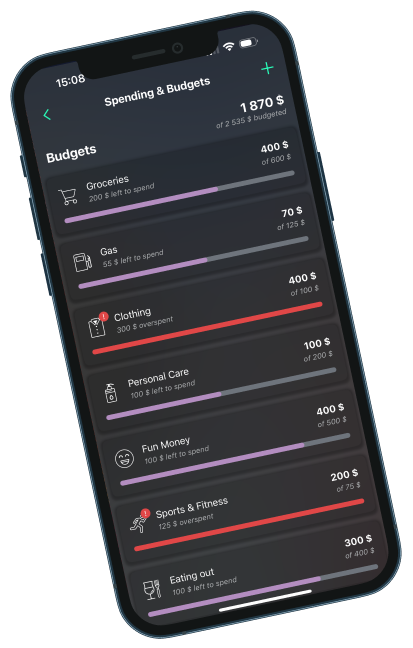

- Budget CalculatorPlay around with your budget numbers to understand where your money is going

- Debt Payoff CalculatorEnter your debt details to calculate an optimal payoff plan tailored to your needs

- 50-30-20 CalculatorSplit your income into needs, wants, and savings with the proven 50/30/20 rule

- Auto Loan CalculatorEstimate your monthly car payment and total financing costs

- Boat Loan CalculatorCalculate what your dream boat will really cost with interest and fees included

- Construction Loan CalculatorEstimate construction costs, draws, and interest for your building project

- HELOC Loan CalculatorEstimate your available home equity credit and monthly payments before applying

- Land Loan CalculatorSee how land purchase costs stack up with interest rates and loan terms factored in

- Motorcycle Loan CalculatorUnderstand the true cost of bike ownership before financing your next ride

- Payment Loan CalculatorQuickly estimate monthly payments and total interest for any personal loan

- Rent Affordability CalculatorDetermine affordable rent based on your income and savings goals

- Student Loan CalculatorEstimate your monthly student loan payments and see your total repayment timeline

- Learning

- PFM CourseLearn more about personal finance, from budgeting mistakes to debt management

- For TeachingUse PocketGuard to help your clients to reach their financial goals

- For CoachingCollaborate with your clients using PocketGuard Advisor platform

- Resources

- Get Started RightSet up your account by following simple steps and recommendations

- Help CenterFind out more info about how to use PocketGuard and how it works

- SecurityLearn more about security measures and your data protection

- NotificationsGet weekly reports and alerts for fees, upcoming bills, and budget progress

- BlogRead articles on personal finance, savings tips, and more

- What’s NewCheck back here for the latest updates to PocketGuard

- AboutLearn more about who we are, our mission, and what we value

- For Business

- API IntegrationIntegrate PocketGuard to enhance user retention and engagement

- Affiliate ProgramBecome our partner and earn more money by acquire more people to PocketGuard

- White LabelGet your budgeting app powered by PocketGuard to improve your business

- Pricing